The ABCs of IRAs

by Sarah Spearman | Hellam Varon

This is the first installment of a three-part series on getting to know the different types of IRAs and the advantages and rules for each of them.

IRAs, also known as individual retirement arrangements, are personal savings plans that provide a tax-deferred method of saving for retirement. Traditional IRAs are sometimes called ordinary or regular IRAs. We will cover both Roth IRAs and inherited IRAs in our next two newsletters.

An IRA can provide tax advantages for setting aside money for retirement. Contributions made to an IRA may be fully or partially tax deductible. Also, amounts inside the IRA (including earnings and gains) are not taxed until they are distributed.

Contributions

For 2017, IRA contributions are limited to the lesser of $5,500 or your compensation. If you are 50 or older, an additional catch-up contribution of $1,000 is allowed. Contributions made in excess of these limits may be subject to penalty or additional tax. Contributions must be made to your IRA by the due date for filing your tax return, not including extensions. For most people, this means that 2017 contributions must be made by April 17, 2018.

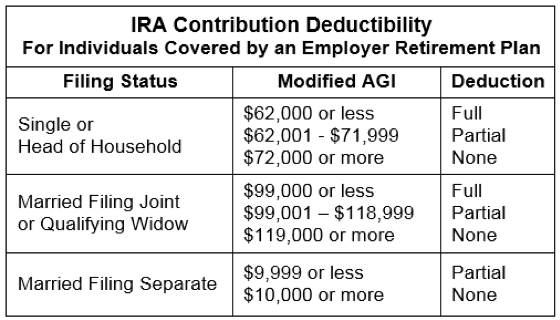

Claiming a Deduction

If the taxpayer wasn’t covered by an employer retirement plan, contributions to an IRA are fully deductible. However, if the taxpayer was covered, the deductible portion of the IRA contribution depends on the taxpayer’s filing status, modified AGI, and, if married, coverage status. See the following table:

It is important to note, even if the deduction is limited, the taxpayer can still make the maximum allowable contribution. This results in a partial IRA deduction and a partial nondeductible contribution.

Required Minimum Distributions

Annual required minimum distributions (RMDs) must generally begin starting the year the taxpayer reaches 70½. Taxpayers may, however, delay the receipt of the first distribution until as late as April 1 of the year following the year they turn 70½. If the first distribution is delayed, it is important to note that the second year’s RMD must also be withdrawn in the same year, resulting in more taxable income. RMD rules are dramatically different for inherited IRAs and Roth IRAs, which we will discuss in later articles.

The tax rules governing retirement benefits are very complex. We have provided the basics here but it is easy to stumble over these rules. Let us help you avoid doing so — give us a call if you need assistance.

Sarah Spearman

Sarah Spearman has been providing tax planning and compliance services to individuals and closely-held businesses since joining Hellam Varon in 2008. She assists her clients in all phases of business and wealth planning, including income tax planning, estate and gift tax planning, resolution of IRS tax disputes, and consulting on a broad range of business issues.

Sarah Spearman has been providing tax planning and compliance services to individuals and closely-held businesses since joining Hellam Varon in 2008. She assists her clients in all phases of business and wealth planning, including income tax planning, estate and gift tax planning, resolution of IRS tax disputes, and consulting on a broad range of business issues.